Insurance is the transfer or sharing of risk from one party or group to another in exchange for payment. This concept is ancient and has been traced back and as far afield as to China and Mesopotamia. In China, farmers faced the challenge of transporting rice crops downriver to market. With one out of ten vessels typically losing its cargo, farmers pooled their resources, contributing one-tenth of their crops to support each other in case of a loss. Similarly, camel trains operated by merchants carrying goods across deserts were subject to robbery and weather losses. They too supported each other in a similar way. This early form of insurance highlights a need that underpins insurance today:

1. Identified Risk: The potential loss of cargo.

2. Financial Risk: The loss of profits from the damaged goods.

3. Risk Group: A collective of individuals or businesses with similar characteristics, in the above example, case,

farmers or merchants.

4. Risk Transfer: Contributing a portion of crops or goods as an early form of indemnity to mitigate losses.

These same principles apply to the insuring of offshore emergency evacuations by helicopter:

1. Identified Risk: The need to evacuate an employee due to a medical emergency.

2. Financial Risk: The erosion of profits, from the unexpected cost of the helicopter flight.

3. Risk Group: Employers with employees working in remote or offshore locations, who take their underlying

health risks with them.

4. Risk Transfer: Purchasing a HeMEP policy (Helicopter Medical Evacuation Program) to cover the emergency

flights, not covered elsewhere.

While a company cannot control the inherent risks associated with its operations, it can manage the risk by purchasing insurance. The decision to buy insurance requires a careful analysis of evaluating one’s own financial strength without insurance to bear the loss, versus the ability to purchase an insurance policy to manage the loss.

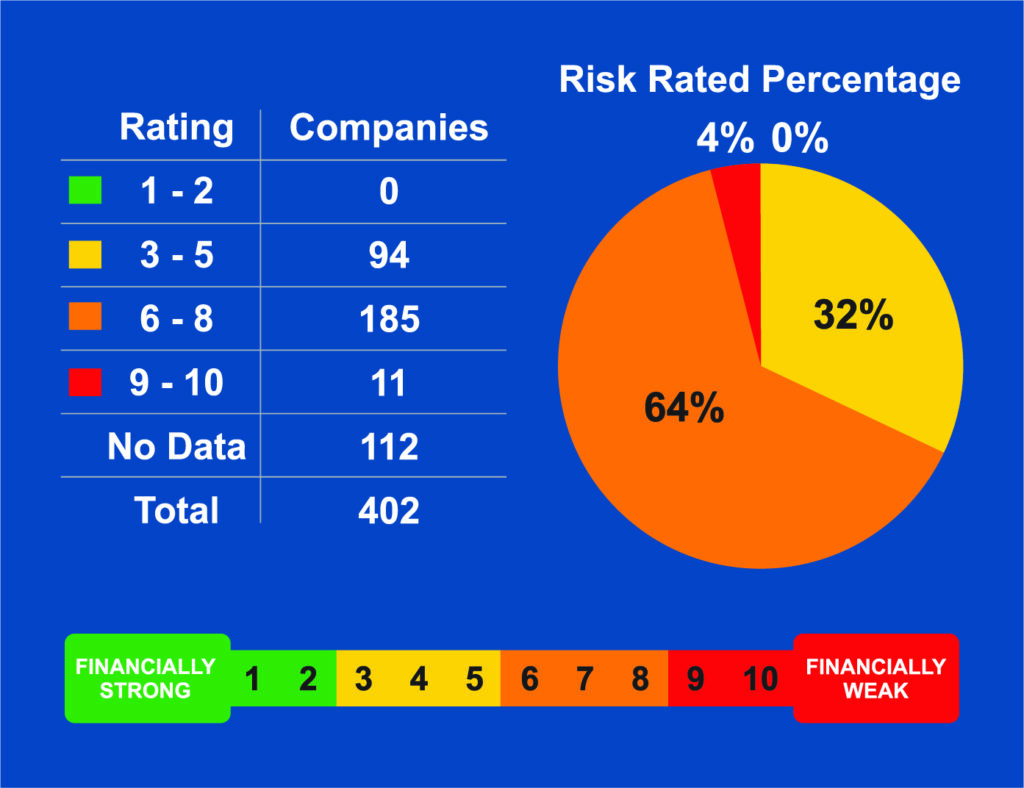

In 2019, HeloEvac worked with an oil and gas operator and conducted a financial assessment of their vendors to establish whether their vendors could afford a typical helicopter flight invoice arising from an unforeseen health event. Using services from Euler Hermes, a financial health check was conducted, rating companies on a scale from 1 to 10, where 1 represented strong financial stability (similar to companies like Microsoft and Walmart), and where 10 was an indicator of financial weakness, possibly nearing bankruptcy. The results were revealing. Of 402 vendors, 68% would not have been able to afford an unexpected emergency helicopter flight cost.

The results underscored the importance of understanding a company’s financial strengths and weaknesses when considering insurance. But, more importantly, showed that most, some 68%, would struggle to pay an unexpected cost of the magnitude of a helicopter invoice from a medical evacuation. We say that a HeMEP policy can be the difference between ensuring that critical, unexpected costs are covered without jeopardizing the company’s overall economic health.