As we and Lloyd’s of London mark one year of issuing policies, numerous discussions have taken place with operators, brokers, contractors, and policyholders regarding a critical shift in contractual language within Master Service Agreements (MSAs) between operators and their contractors.

Increasingly, we see amendments to MSAs that now include clauses requiring contractors to bear financial responsibility for medical evacuations. This change addresses a long-standing gap in offshore risk management for both operators and contractors. While it mitigates financial exposure for operators, it leaves contractors vulnerable to the substantial costs of non-work-related medical emergencies. This is a change for the benefit of all parties as the MSA will now clarify who is financially responsible. For a work-related medical flight, both the operator and the contractor will have insurance in place for such costs under their respective workers’ compensation insurance.

However, for a non-work-related medical flight, workers’ compensation insurance will not provide coverage. When the Helicopter Medical Evacuation Program (HeMEP) and its accompanying insurance policy with Lloyd’s of London launched in February 2024, the goal was to address this gap in insurance coverage. The intent was to bring attention to coverage limitations and contractual ambiguities in the Gulf of America while providing an affordable insurance solution. However, recent MSA requirements still leave a crucial issue unresolved: the need for a practical, equitable, and cost-effective solution backed by insurance.

While the updated language in MSAs is a step in the right direction, it does not fully resolve the issue, lacking an insurance component.

Operators have only done half the job if they make contractors responsible for the cost of non-work-related medical evacuations but do not require insurance to cover such exposure in their MSAs. If contractors are expected to bear the financial burden of medical flights for their employees, they should also be required to have insurance for that liability. Anything less fails to truly address the issue.

Medical Flights—Who is Responsible

Platform safety is ultimately the responsibility of the operator. This remains the case regardless of who calls for a medical flight. If the operator requests a flight for their own injured employee, they will pass the cost of the medical flight to their workers’ compensation carrier. However, the workers’ compensation carrier will only cover the flight if the injury is work-related. If the injury is not work-related, the operator has no coverage, making it an uninsured liability.

If the operator requests a flight for an injured employee of a contractor, the new clauses in the MSA place the cost burden of the flight on the contractor. Similarly, the contractor will pass the cost of the medical flight to their workers’ compensation carrier. The workers’ compensation carrier will only cover the flight if the injury is work-related. Again, if a non-work-related condition necessitates the flight, it becomes an uninsured liability. If the contractor cannot afford this uninsured liability, the contractual risk transfer does not protect the operator.

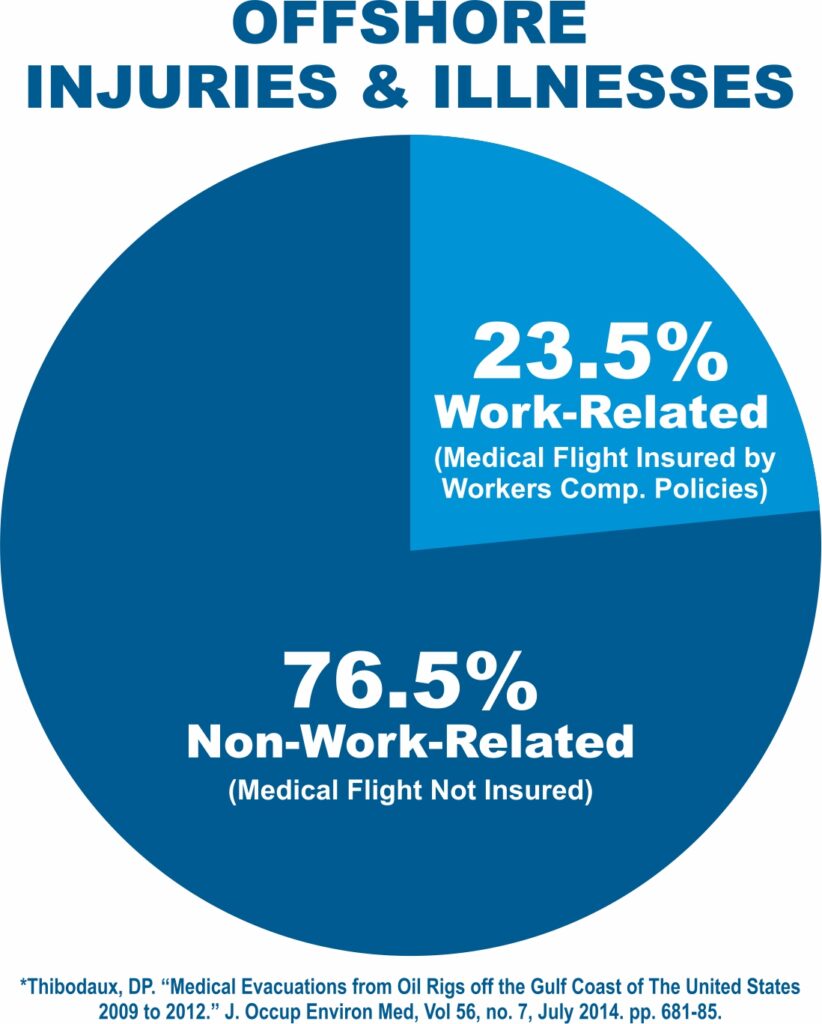

Our data shows that between 75% and 90% of all medical flights arise from non-work-related injuries. This means that in 75% to 90% of cases where a contractor requires a medical flight, it will be an uninsured expense for them to cover, as now mandated by the MSA.

In short, if the operator is mandating the contractor to purchase workers’ compensation insurance, which will cover work-related flights, then why not mandate the purchase of HeMEP coverage for non-work-related flights?

Common Considerations

The following are the ten most common considerations for either the operator, contractor, or both when evaluating the requirement of the HeMEP Policy.

1. Friction arising from the contractor’s inability to pay.

Most contractors will be unable to meet their obligation under the MSA to cover medical evacuation costs without insurance. Since they lack coverage for a medical flight 75–90% of the time, this creates a disconnect between the operator and the contractor. Multiple instances have been observed where contractors were financially shorted on their invoices with operators, allowing operators to recoup the evacuation expenses.

2. Contractual ambiguities and accountability

Today, if a question arises regarding who is responsible for evacuation costs, both the operator and the contractor are at risk of a dispute forming between themselves over any ambiguities in the MSA. This can result in the potential for bad feelings or in a worst-case scenario, the prospect of legal proceedings.

To prevent these issues, MSA language should be clearly defined, and payment provisions should be explicitly outlined. This clarity helps avoid conflicts, protect financial interests, and ensure smooth operational processes without unexpected liabilities. Both the operator and the contractor will refer to the MSA to determine liability and the process for cost settlement, which is typically addressed through insurance provisions and insurance like the HeMEP policy.

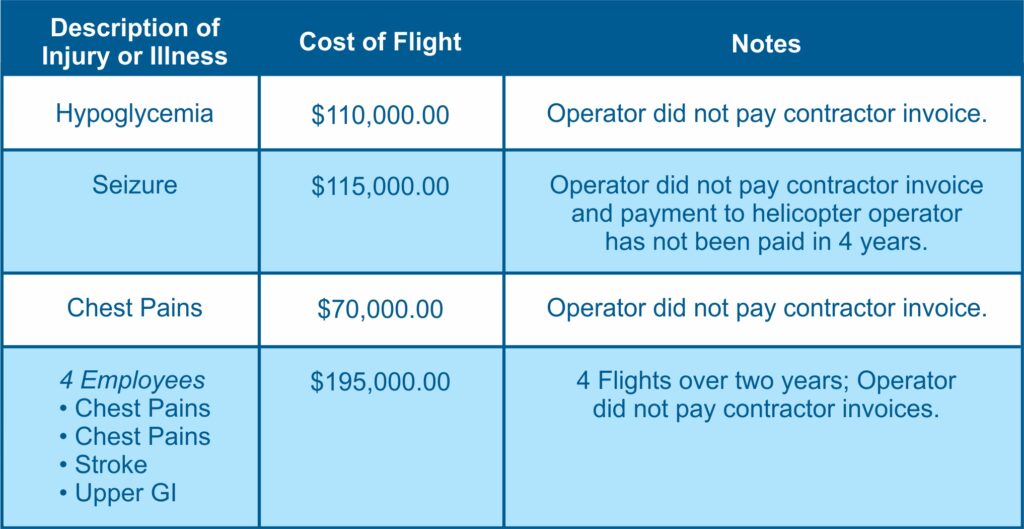

3. Uninsured flight costs are expensive and are difficult to afford

A typical flight is around $85,000. In the table below are some real-world examples of flight costs and outcomes.

It is settled data that most contractors cannot meet an unexpected and uninsured cost of $85,000 as it falls due. The HeMEP Policy will keep the contractor in business.

4. Unpaid Medical Flight Providers

When a medical flight provider goes unpaid, understandably the medical flight provider will unlikely fly again for either that operator, that contractor, or that location. This limits further an already scarce resource available to operators and contractors alike. In circumstances where a medical flight provider is charitable in agreeing to fly again for an operator or contractor or location that previously had not paid for a flight, they will not do so without a credit card being provided in advance. If the provider of the credit card is the operator, they will face the same reimbursement challenges as the flight provider. A workers’ compensation carrier will not cover the cost of a non-work-related flight whether for their employee or a contractor’s employee.

5. Delayed Medical Response

In the absence of appropriate insurance coverage, delays in arranging timely medical evacuations are inevitable, as each flight request may be unplanned and unfamiliar to the caller. There may also be hesitation about whether the flight is truly necessary. By purchasing a HeMEP policy, the insured is automatically enrolled in HeloEvac. HeloEvac provides a 24/7 toll-free hotline that anyone can call in the event of a medical emergency. This eliminates uncertainty and allows the caller to appropriately defer responsibility to an independent medical professional at HeloEvac. If the medical professional determines that a flight is necessary, HeloEvac will cover the cost upfront, regardless of whether the flight is work-related or not.

6. Does the Marcel Exception assist the operator with medical emergency flights?

It does not. The Marcel Exception allows an operator to contribute premium money to a contractor’s liability insurer to add the operator as an Additional Insured under the contractor’s liability insurance policy. However, the exception does not apply in this case because an operator cannot be named as an Additional Insured under a Workers’ Compensation or HeMEP policy. Therefore, the Marcel Exception does not apply to “expenses-only” policies such as the HeMEP policy.

7. Does the HeMEP Policy Support Compliance?

Yes, it does. BSEE Safety Alert No. 469 (October 20, 2023) highlights significant compliance gaps in medical support, evacuation procedures, and emergency response capabilities across offshore facilities in the Gulf of America.

During a Performance-Based Risk Inspection of 20 production and well operation sites, including 12 production facilities and 8 well control facilities operated by 15 different companies, BSEE inspectors identified:

- Inconsistent documentation of injuries and illnesses.

- Procedural gaps and flaws in working practices.

- Deficiencies in medical support and evacuation resources, leading to delayed or failed emergency responses.

It made the following findings:

- The average time from incident occurrence to hospital arrival was 6.8 hours, a delay that could impact patient outcomes.

- Medical supplies were inadequate, and many offshore workers did not know where first-aid kits were located or how to use them.

- Emergency action plans were outdated, difficult to locate, and contained incorrect contact information. In some cases, only the person in charge knew the plan—posing a major risk if they became incapacitated.

- Many operators could not provide proof of regularly conducted medical emergency drills, despite regulatory requirements.

By purchasing a HeMEP policy, the insured is automatically enrolled in HeloEvac, which provides:

- A 24/7 toll-free medical emergency hotline, ensures immediate access to medical guidance.

- Prepopulated call sheets for offshore phone sites, simplifying emergency calls.

- Annual medical emergency drills at production and well control facilities, fulfilling regulatory requirements. A HeloEvac subscription directly addresses the compliance shortcomings identified in the BSEE Safety Alert and significantly strengthens emergency preparedness for offshore operations.

8. Is there increased operational costs for the operator if it requires the HeMEP Policy?

Requiring the HeMEP policy has minimal financial impact compared to the significant risk of not having medical evacuation coverage. If operators do not clearly define responsibility for medical flights in the MSA, they remain fully liable for evacuation costs, leading to unexpected and potentially substantial expenses.

Mandating HeMEP coverage for contractors does not inherently increase costs for operators. Many contractors already account for insurance increases in their pricing models, just as they do for health insurance, workers’ compensation, and equipment costs. Additionally, operators can stabilize their expenses through fixed-pricing agreements.

The cost distribution model of HeMEP makes it highly efficient. For example, a $12,000 annual premium split across four contracts results in just $3,000 per contract, which is only 0.6% of a $500,000 contract.

Beyond cost efficiency, HeMEP simplifies financial processes:

- It pays upfront for both work-related and non-work-related evacuations, eliminating flight invoices and reimbursement tracking.

- The policy is tax-deductible for both operators and contractors, reducing the net cost.

- HeloEvac secures exclusive pricing through alliance partners, ensuring that flights booked through the program are often more cost-effective than standard market rates. Overall, the HeMEP policy provides cost predictability, protecting both operators and contractors from high, unexpected medical flight costs, while also fostering stable, manageable pricing.

- For those operators that use ISNetworld, ISNetworld can include the HeMEP policy to assist with rollout before the MSA is signed and to manage the implementation of the HeMEP policy thereafter.

- And, there is no deductible to pay under the HeMEP policy

9. Is it prudent to “roll the dice” and simply run the risk and self-insure?

No. Our data suggests there are roughly 400 emergency medical flights per year, so between 300 and 360 are for non-work-related maladies. Frankly, the offshore workforce continues to age, and they take their health risks with them when they go to work. It seems it is not a matter of “if” a flight will occur and more a matter of “when”. It is also ill-advised to believe that once a company has a flight, they are unlikely to have another. We have several examples of a single company having multiple medical emergency evacuations in a single year. It is one of the driving factors that allows a HeMEP insured to repurchase limits in a policy year after they have had an insured flight. Lastly, the litigation risk of not being insured, resulting in a flight delay, might be exacerbated since the coverage exists and includes a simple emergency medical assessment.

10. Compliance

Compliance with Safety and Environmental Management System (SEMS), OSHA, BSEE, EPA, BOEM, and other applicable standards are closely tied to ensuring proper insurance coverage and wording in MSAs. Compliance therefore helps mitigate financial burdens and improve safety. Health, Environmental, and Safety departments depend on various insurance policies, such as water pollution, auto, worker compensation, general liability, and others like equipment and property damage coverage, to mitigate financial burdens and improve safety. Using insurance is the accepted solution to mitigate financial burdens and to improve safety. A part-way measure that fails to require a HeMEP policy to fill the gap in insurance simply fails to solve the financial burden and does nothing to improve safety, in fact, it makes the contractor’s employees less safe since they cannot rely upon HeloEvac. We say that this part measure exposes both the operator and contractor to the financial burden despite the attempt to apportion it under the MSA. If a medical emergency occurs without access to HeloEvac, the employee’s safety is severely disadvantaged.